Macro Matters

Macro Matters

Macroeconomic factors can explain 75% of stock market return variation.

Macro Matters: Why Macroeconomics is Essential for Investors Today

It's easy to forget that the stock market is driven by forces beyond individual companies. However, it's crucial to remember that forces beyond individual companies exert a powerful influence on the stock market.

What Does Wall Street Priortize in their Analysis?

Macro is Underemphasized Overall.

Bottom-up analysis dominates top down on Wall Street. Where 34.8% of S&P 500 Stories reported on Bloomberg have been focused on Earnings, while only 3.2% is focused on Macroeconomics. 1

Currently, Most professionals believe that idiosyncratic risk or company specific influences is what matters most when gauging the risk reward for equities.

Surveys reveal a surprising trend: Wall Street analysts remain fixated on fundamental analysis, prioritizing factors like earnings over crucial macroeconomic drivers such as price-to-earnings ratios. This micro-focus has led to underperformance, with only 32% of U.S. fund managers consistently outperforming their benchmarks over the past decade, driving a shift towards indexed investment strategies.

While various explanations for this underperformance exist, two critical factors are often overlooked: the profound impact of macroeconomics and the lack of macroeconomic expertise among investment professionals.

Traditional finance education heavily emphasizes bottom-up fundamental analysis, neglecting the top-down macroeconomic perspective. This bias is often reinforced by programs like the CFA®, which, while valuable, may overemphasize fundamental analysis at the expense of a broader understanding of macroeconomic forces.

The focus of wall street should be tilted towards macroeconomics

The impact of macroeconomic factors on investment performance is substantial and undeniable. Studies indicate that approximately 75% of stock return variation can be attributed to macro forces [see @greenwald_origins_stock_market_fluctuations]. Yet, a disconnect persists between this reality and the prevailing practices in the investment industry.

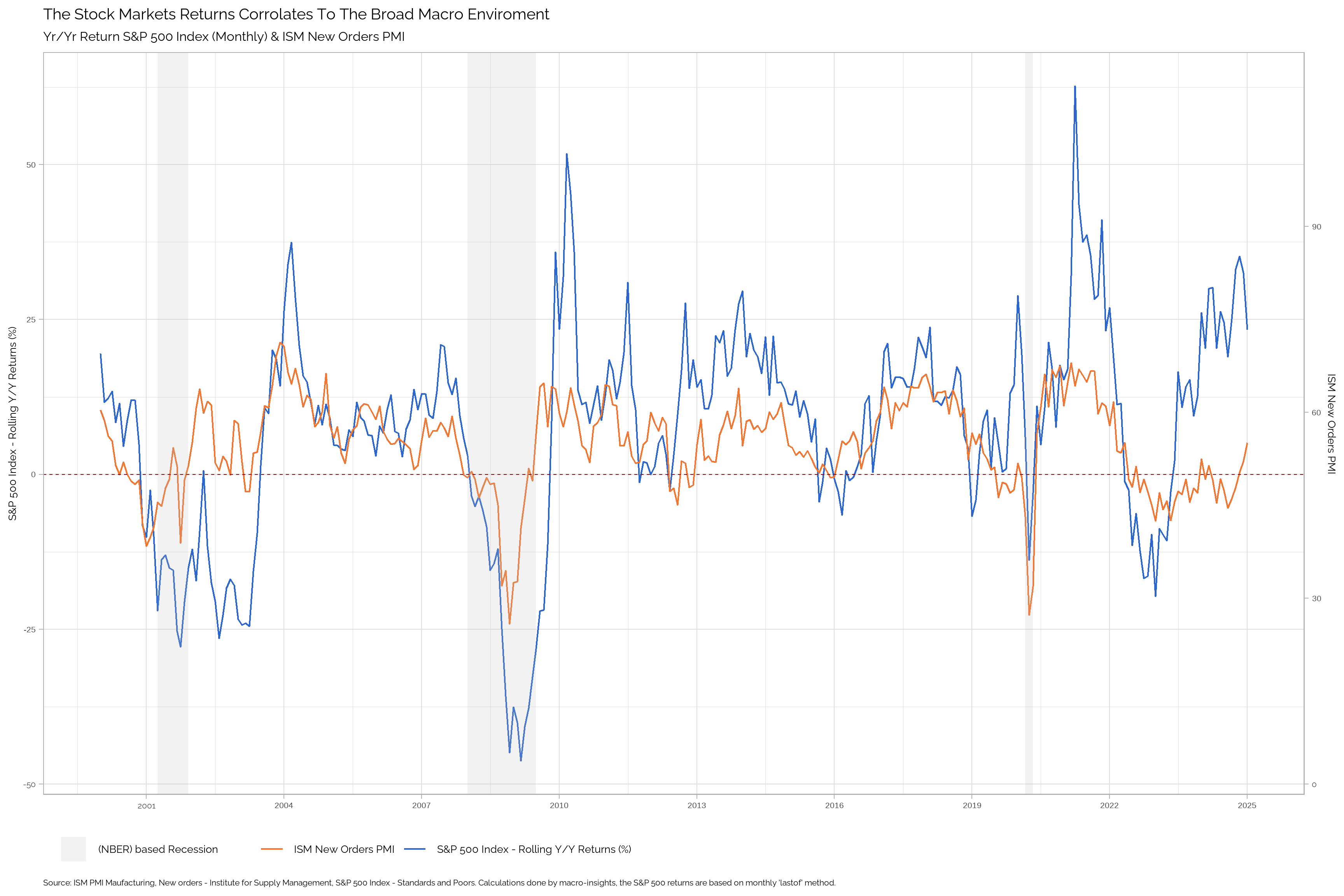

The correlation between stock market returns and macroeconomic indicators is undeniable. As illustrated in the chart below (Figure 1), the ISM Manufacturing New Orders Index, a key gauge of economic activity, exhibits a strong relationship with the rolling returns of the S&P 500.

This chart highlights the interconnectedness between the real economy and financial markets. The ISM New Orders Index, by reflecting changes in manufacturing activity, provides valuable insights into the health of the economy. As the index rises, signaling increased economic activity, stock market returns tend to follow suit. Conversely, when the index declines, suggesting a potential economic slowdown, stock market returns often reflect this downturn.

This clear link between a macroeconomic indicator and stock market performance underscores the importance of incorporating macroeconomic analysis into investment strategies. By understanding the dynamics of the broader economy, investors can better anticipate market movements and make more informed decisions.

This disconnect is a significant oversight. To achieve superior investment outcomes, a robust understanding of macroeconomic cycles, trends, and policies is essential. Integrating macroeconomic analysis into investment strategies allows for:

- Proactive Risk Management: Anticipating economic turning points and adjusting portfolios accordingly.

- Enhanced Return Generation: Identifying opportunities aligned with the prevailing macroeconomic environment.

- Improved Client Communication: Providing clear, macro-driven rationales for investment decisions.

The investment industry must bridge this knowledge gap by prioritizing macroeconomic education and integrating it into investment processes. By recognizing and harnessing the power of macro, we can elevate portfolio management from mere speculation to a more informed and effective discipline.

Shorter Investment Horizons Enhance The Role Of Macro

The relationship between the stock market and GDP growth further emphasizes the importance of macroeconomics in today’s investment landscape. As shown in the chart below (Figure 2), the S&P 500 tends to lead U.S. GDP growth by approximately six months. This suggests that investors can gain a competitive edge by anticipating economic turning points based on stock market movements.

This relationship has important implications for investors, particularly in light of the trend toward shorter holding periods. As holding periods decrease, the impact of cyclical economic fluctuations on investment returns becomes more pronounced. By understanding the cyclical relationship between the stock market and GDP growth, investors can better anticipate economic turning points and adjust their portfolios accordingly.

For example, if the stock market begins to decline while GDP growth remains robust, it could signal an impending economic slowdown. This would suggest a more cautious investment approach, potentially reducing exposure to equities and increasing allocations to more defensive assets. Conversely, if the stock market shows strength while GDP growth is lagging, it might indicate an upcoming economic recovery, presenting opportunities for investors to capitalize on growth-oriented investments.

In essence, the stock market acts as a barometer of future economic conditions. By integrating macroeconomic analysis into their investment process, investors can gain a forward-looking perspective, enabling them to make more informed decisions and navigate the complexities of a dynamic market environment.

The investment landscape has changed

Equities are inherently long-term instruments. While their value can fluctuate significantly in the short term, with declines of 10% to 20% or more not uncommon, a long-term perspective—spanning years or even decades—allows investors to weather these market fluctuations and potentially achieve superior returns.

Historical data supports this view. Since the 1920s, a 20-year investment in the S&P 500 has rarely resulted in losses [see @macrotrends_sp500_historical_annual_returns]. Even during tumultuous periods like the Great Depression, Black Monday, the tech bubble, and the 2008 financial crisis, investors who maintained a 20-year holding period ultimately experienced gains.

This highlights the crucial role of investment time horizon. However, the investment landscape has undergone a dramatic transformation. In the 1960s, the average holding period for stocks was around eight years, emphasizing the importance of structural factors in investment analysis (see Figure 3). Today, with holding periods of six months or less, cyclical forces have become the dominant driver of returns.

This shift has profound implications. A longer holding period, such as eight years, diminishes the influence of the business cycle, allowing investors to focus on fundamental analysis and long-term company performance. Conversely, shorter holding periods, characteristic of today’s market, amplify the impact of macroeconomic forces on stock prices.

Despite this evolution, financial education often remains anchored in the past, geared towards a world of extended holding periods and a focus on fundamental research. This disconnect between traditional training and the realities of today’s market necessitates a shift in emphasis towards understanding and navigating cyclical forces.

The question then becomes: how can investors thrive in this environment where the tides of the market turn with increasing speed? The answer lies in a dynamic approach, one that marries the enduring principles of fundamental analysis with a keen understanding of cyclical forces. By recognizing the interconnectedness of economic cycles, monetary policy, and market sentiment, investors can position themselves not merely to survive, but to capitalize on the waves of change. This demands a new breed of investor, one equipped not only with financial acumen but also with the tools and insights to navigate the complexities of a rapidly shifting landscape.

This new era demands investors who possess not only financial acumen but also the ability to interpret the signals of an increasingly complex and interconnected global economy.

Footnotes

Research done by Trahan Macro Research LLC, from 2018 - 2022 (c)2022, allrightsreserved↩︎